Here is today’s summary of the “Campfire Talks with Herbie”.

TameFlow Community Member: Cherifa Mansoura

Name (and Company/Affiliation if desired)

Who are you?

Born and raised in Algeria, in a small village called Sfisef. I had my Computer engineering degree and then moved to England/Leeds for my PhD (in the field of knowledge representation). I spent around 10 years studying and working as a consultant in the OOAD (Object Oriented Analysis and Design) space. I moved to Canada in 1997 where I started my first job as an Associate professor with the University of Winnipeg as well as doing part time consulting with a small company. One day, by curiosity, I went to a computer fair and dropped my CV with the IBM booth. 2 days later I had a call asking me for an interview. Soon after, I received an offer for a Business Analysis job.

For +16 years, IBM was a school to me.

Today I am Agile Transformation Coach, change agent, and consultant working with organizations, leaders and teams, providing guidance and coaching around lean and agile practices. I mentor team members and leadership on how to transition to a better way of working and provide them with all means of improvement. I collaborate with people across widely varying levels and roles, leading teams toward further understanding and adoption of Agile as well as overall company growth and improvement. I develop and design strategies for the organizational adoption of agile and this includes every stage of the adoption

How did you get involved with Agile, Coaching, Organizational Performance - and in particular with TameFlow?

Let me start with Agile

I got involved with the new ways of working while I was working with IBM and consulting with clients who were seeking the adoption/implementation and customization of RUP (Rational Unified process). During this period (early 2000), various companies were leaning towards this approach but found it heavy in terms of number of roles, artifacts and activities. We as consultants, started looking into lighter configurations with several customers: I have spoken in a conference back in 2005 on how to “Agilize RUP”. End of 2005, still with IBM, there was a company who was more interested into DSDM (Dynamic system Development Method) and wanted us to come up with a hybrid approach combining the best practices of DSDM and RUP. This engagement was an eye opener in terms of how companies started embracing some agile practices. From a learning perspective, it was very successful, the client was happy. Rational IBM started reviewing their suite of products strategy to align them well with lean and agile practices. In 2008, as a program manager I led the development of the Agile Service Offerings within Rational. From there, emerged a self-check tool for agile assessment, the Disciplined Agile Delivery framework, a process template for the agile planning and collaboration tool such as RTC. I was a solid contributor for those three assets. With a team of 10 people, we developed training. I enabled more than 300 team members worldwide (from Colombia to Brazil, France, Germany and India). Between 2008 and 2012, I was engaged with several companies WW during their agile transformation where DAD was the framework of choice at that time.

Now with TameFlow, it is not that long: to tell you the truth. I was not aware of this approach. My connection on LN with Daniel, allowed me to see some of his posting. One day, I asked him if you could be a presenter for the group Women In Agile Montreal (WIAM) that I am leading. He accepted and from that day (June 22nd) he introduced us to the TameFlow Approach, I became more interested. I searched for your book and got an online version in our national library. I am still reading it.

Are you currently (or do you intend) making a living in this sector? And with TameFlow?

In the agile space, I started as a consultant with IBM. I got hired by Teksystems back in 2014. I was one of the first agile consultant helping Teksystems to develop a SDLC engagement model, inspired by DAD. I enabled several teams on how to go about using this model on a solution delivery. I then moved to the ATS (Agile Transformation Services) practice and worked with several clients on their transformation, using various frameworks. Today, I am back to revive my own company which I created in 2013. and intend to make a living providing consulting, training and advisory services in the lean and agile space. I will continue to provide coaching for organizations who seek guidance and help for their transformation. I am newbie for the TameFlow Approach. I have plans to educate myself. Adding this approach to my tool kit will certainly equip me well to the various choices I will bring to my clients.

Give us a typical day in your life!

Typically, I have a breakfast around 7-8:30 am. I prepare a nice tray with fruits, oatmeal and a drink with lemon juice. I take the time to finish my breakfast and next step is to prepare a coffee (with an Italian coffee maker). I drink my coffee while watching one of my favorite show on itv-yorkshire (Loose Women). I make my bed.

I will serve myself another small coffee and sit on my chair, in front of my computer. I then check my emails, while still sipping my coffee in front of the TV. That gives me enough energy to start my day.

I will then think about my daily plan. Sometimes I track my items on a piece of paper the night before and when that happens, I will review it first thing first and see if I need to make any changes. Since I moved from my last job, I spend time preparing content for my website, attending webinars, writing, reviewing work done by others, revising my CV, etc.

When I am tired of sitting more than 1 hour on my desk, I take a break and do something around the house (washing dishes, reading my snail letters). Later during the pm and after a lunch, I will may make myself a cup of tea.

Mid and end of day, I check my list and cross the activities that I have completed (usually two or three key items).

At 5pm I go for an hour jog and if I need something from the shop, I will buy it on my way. Back home, I will water the plants outside (I planted some flowers during this summer to keep me going). I will shower, have dinner and if any other activities are to be done using my computer, I will have it this time on my lap. By 8pm, I will make another tea, sit and relax in front of the TV.

My pre-bed ritual is to read few pages of a book and sleep.

What makes you happy at the end of a day?

When I make a difference in someone’s life during the day. I enjoy giving back whether in the field or in daily routine.

-

It can be work related such as responding to questions on SAFe blog or anything else, women in agile finding a speaker, scheduling a presentation. Delivering a presentation, reviewing papers, being a member of a thesis jury, mentoring other people

-

When it is not work related, I feel a sense of satisfaction when I help the homeless. As an example, just next to where I live, there is a water spray and every time when I go through that park, I see homeless people taking showers or just refreshing themselves. However, they never seemed to have towels. So about 2 weeks ago, it was around 40 degrees Celsius and I decided to take towels from my home (6) and distributed them. I really felt a sense of fulfillment

-

Family related, I am so happy to see my girls and face time with my two grandsons at the end of the day (Dolly is Mia’s dog and Eden, 18 months old, is Noumy’s son). I do not see them very often f2f (especially at this time of the pandemic) but when they come through the door, I see a big smile on Eden or Dolly’s face (yes Dolly smiles too!!).

What’s the most important skill or insight you’ve developed while getting involved with this industry?

Where to start? As an old timer in the industry, I have developed so many competencies. I always maintain a spirit of continuous improvement and I am constantly learning. And more, I think I know how to maintain a balance to be able to determine which competencies are more relevant in a certain situation I have developed several passions starting with my business analysis and business architecture career to now as an Agile/lean Transformation lead. As a business BA we master and apply a particular facet of analysis (framework, a methodology, a specific tooling usage model, facilitation and prioritization techniques and ways for communicating with customers/stakeholders. The Business analyst in me played crucial role in guiding enterprises and people in taking the necessary steps to articulate their Vision, change their products, their processes, and their services. As an agile coach, I learned to address the people-side of change. We as People find strength through empathy and understanding. I learned to build empathy for the people I serve. I learned to understand their pain points, goals, and motivations. I needed to understand what’s working today and what isn’t. I needed to avoid projecting or assuming. I needed to quiet my ego so that I can listen better and observe. So, to summarize, one passion led to the other! The Agile transformation Consultant and Coach that I became, has developed further the people, the listening and communication skills.

What are the greatest challenges on your path to using/improving the techniques you favor in this sector? Where do you see TameFlow in this?

-

Poor Leadership can be detrimental and is a challenge when Leaders are not supportive and do not lead by example.

-

I have learned that when companies force a process on people without receiving their commitment to perform, they’ll become resentful and fight change – even when they know that the transformation is worthwhile. This is more about meeting people where they are!

-

Scaling is not very well understood and people think you should only be scaling vertically. Further, Scaling requires a Vision, commitment and clarity on why do we need scaling?

-

When it comes to adopting a particular framework or approach, some consultants do not look into the big picture. Knowing why adopting this framework is very important. A framework is only a “FRAMEWORK”. By essence, it should be adapted to the organizations needs and context. The problem today is that some certifications are promoted and requested by companies. Nowadays, it became easy to get certified without understanding deeply the concepts: what matters most is the certification rather than the body of knowledge and the Why are we selecting this instead of that?

-

As for the TameFlow Approach, I would like to see why the TameFlow Approach instead of Kanban? Kanban has been abused or misused. I do not recommend it as an approach when teams do not have the experience with agile and lean way of working. Practices get distorted. A lot of money is spent to solve the wrong pbs.

-

the TameFlow Approach seems such a powerful approach, I am concerned that it can be misused. the TameFlow Approach thought leaders should prepare the ground for people to grasp the concept, understand the benefits, blend it with the in-house practices (it is not an erase and do it again) and above all understand the Why? Why? In what context the TameFlow Approach can work better? Having a thorough comparison between the TameFlow Approach and other approaches is also a way to educate people and guide them on their selection.

Personal challenge: I feel I need to know something before I can talk about it. I do not deal well with ambiguity. I have to have some clarity on everything and this may be a weakness on my part.

What are the greatest rewards you’ve had (personally or professionally) or would like to receive in this industry?

-

Personally, pursuing a PhD was the greatest reward I have had. I set this goal when I was only 20 years old and never thought I would reach it. After 5 years of tears and joy, I finally checked the box at the age of 40+.

-

Work related; I have had so many rewards in several situations: Most of them are related to engagements with clients. When you contract ends and you are asked to stay longer, those are the type of rewards that you would keep in mind.

-

Further, mentoring people and seeing the results and the progress made in their career paths is also another rewarding situation. For so many years I have mentored aspiring analysts, coaches, product owners and guided them through their learning. This is why the coaching is a just something natural to me. It seems that I I have done it all my whole life

-

Learning from exceptional thought leaders was very rewarding

What do you want to learn from a community of peers, like the one here TameFlow Community site?

I educate myself using various means:

-

Classroom training with real case studies

-

45mn workshops here and there on specific topics (ToC, operational flow, financial flow, psychological flow, etc) and what’s in it for some of the roles (financial, Product manager, etc)

-

45mn webinars to help elucidate some of the concepts, especially a topic such as the “throughput accounting”.

-

Link between Value Stream and flow efficiency metrics with the the TameFlow Approach metrics

-

Mentorship (looking into the peers who can mentor others on the TameFlow Approach)

-

Writing articles and submitting talks by attending conferences. Have visibility in the Agile Alliance community

-

Creating accelerators for people to use when they are in a situation to adopt the TameFlow Approach (How to achieve the unity of purpose, what is the best way to establish the DBR, parallel between Kanban and the TameFlow Approach, more…

-

MORE….

If other TameFlow enthusiasts want to reach out to you, where do they find you? And what is your TameFlow Community handle?

- TameFlow Community: cherifamans

- LinkedIn: Cherifa Mansoura, PhD

- Soon to come: my website!

What question(s) would you like to ask Steve, or what topics would you like him to develop (in relation to the TameFlow Approach)?

-

What if there is no Herbie, would the TameFlow Approach concepts still hold?

-

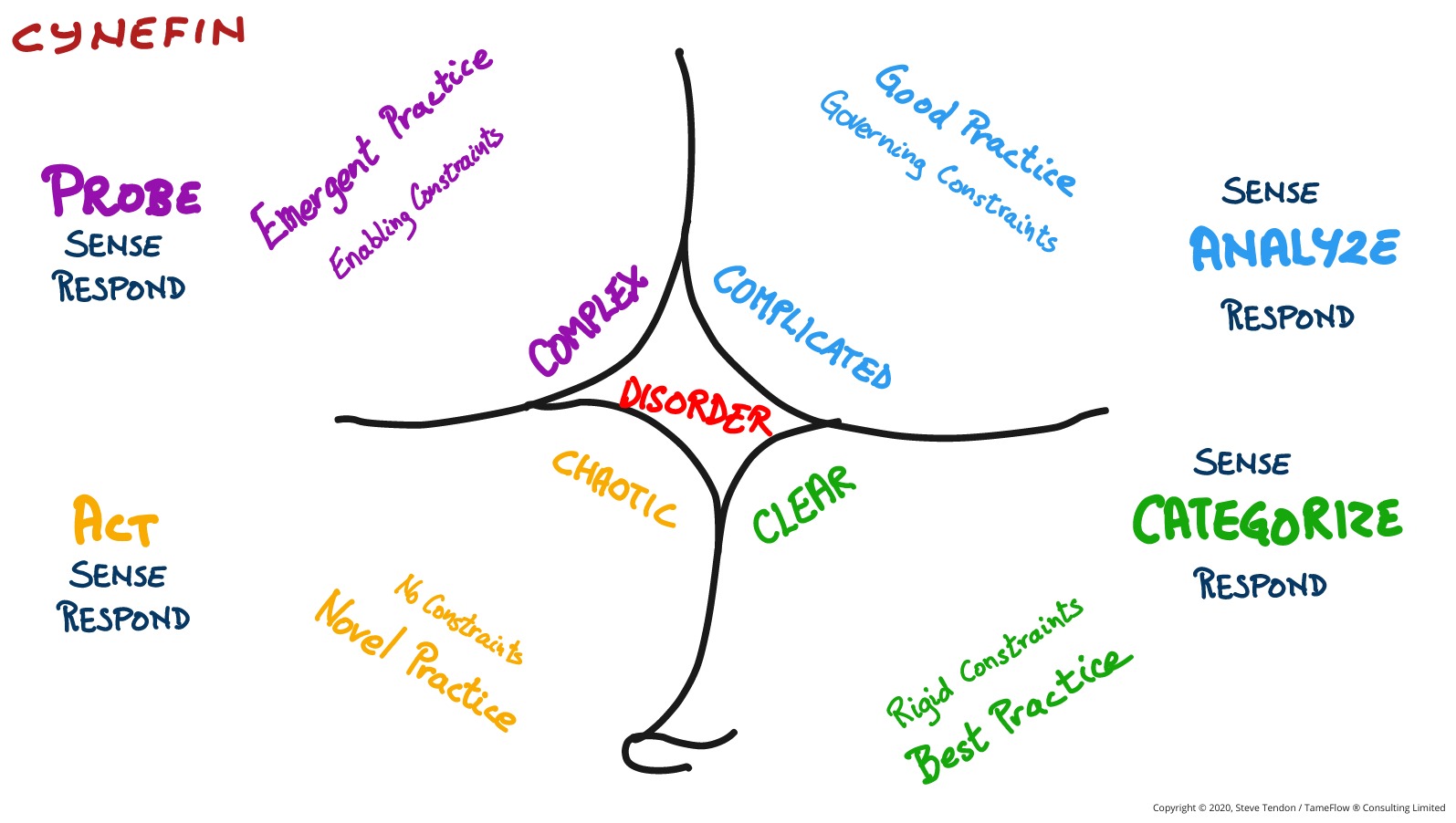

Let’s take the Cynefin diagram. Where do you see the TameFlow Approach thriving?

-

One of the forte of the TameFlow Approach is the Throughput Accounting (TA). “Beyond Budgeting” (BB), on another hand, is something I am interested in (wrote two papers around it) but I never made the link with throughput accounting. Of course, I denounce the cost accounting. I talk about value delivery plus Leadership but I would be curious to see if you have gone through the BB principles and see if you can make the link with TA. Further, how can the TameFlow Approach help make the transition to BB (I believe it can).

Herbie talks about… Cynefin, Beyond Budgeting and OKRs

With reference to the first question, “What if there were no Herbie…?” we take the logical assumption that is the underpinning of the Theory of Constraints: If there were no Constraint then the organization would achieve an infinite amount of its Goal. Since that is clearly not happening, logically there must exist a Constraint.

If we are not able to identify the Constraint, then it does not mean that it does not exist. It is way more likely that we are not able to understand where it is.

Notably this was the reason why the Kanban Method came to be. The impossibility of identifying the Constraint created the expediency of introducing the so-called “Column WIP Limits” (badly mimicking the original Kanban of Taiichi Ohno). The proponents of the Kanban Method clearly stated that it was “impossible” to find the Constraint in knowledge work. With TameFlow we have proven them wrong. They were just not trying hard enough to find it!

TameFlow and Cynefin

The Cynefin Framework is best discovered through the resources of its inventor, David Snowden. We won’t repeat the explanations here. Though as a reminder, let’s keep the following illustration in mind.

Note: Something to keep in mind is that in Cynefin the term “Constraint” is used as well; though the word has a different meaning than what it does in the Theory of Constraints. It could maybe be described as a “Constraining Factor” which can be rigid, governing, enabling or absent.

What is noteworthy is what kind of actions are suggested as fitting the domains. In particular:

-

Clear: Sense, Categorize, Respond

-

Complicated: Sense, Analyze, Respond

-

Complex: Probe, Sense, Respond

-

Chaotic: Act, Sense, Respond

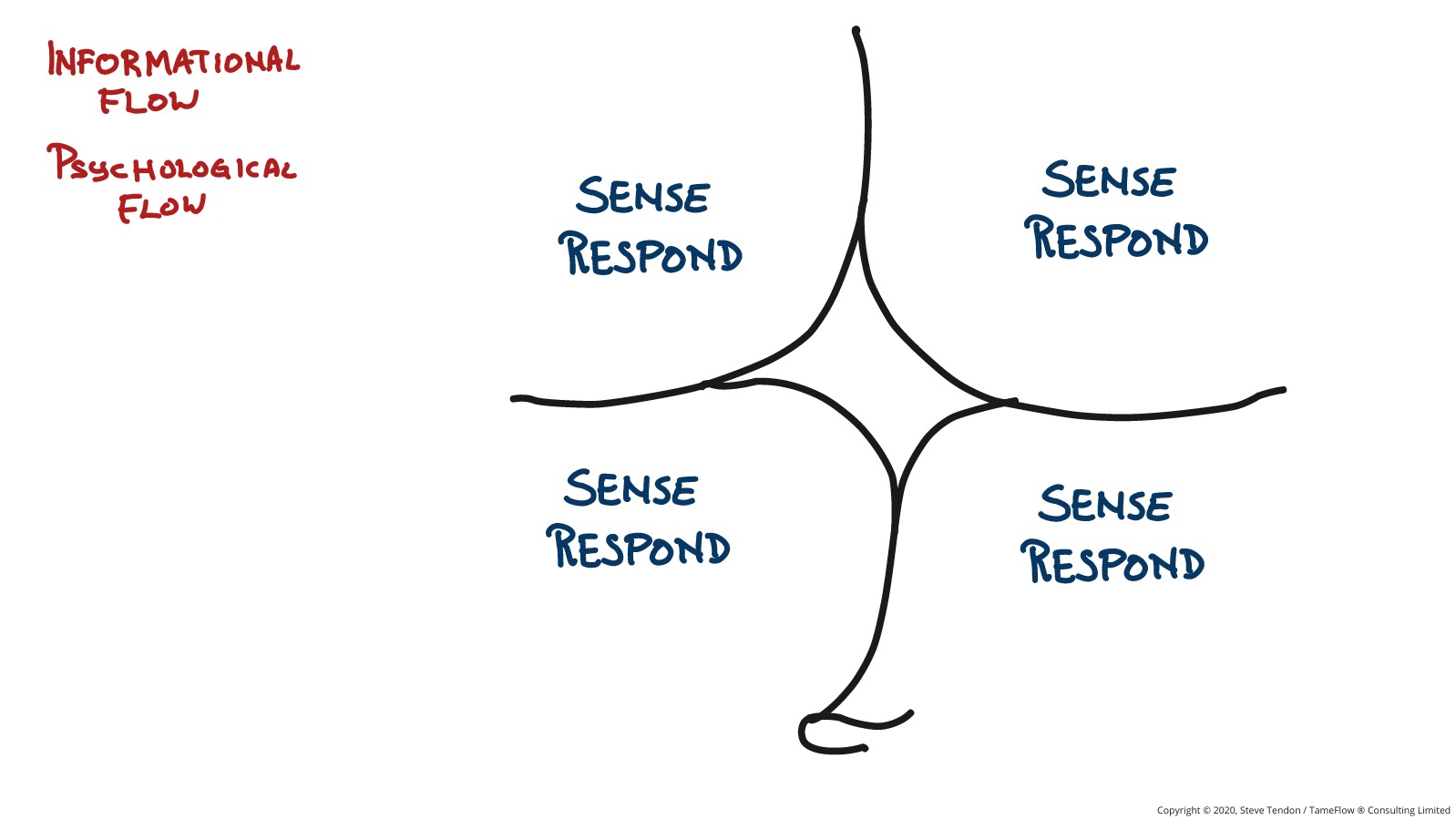

We highlight how in all four cases it is necessary to “Sense” and “Respond.”

In the TameFlow Approach there are many elements that improve the Informational Flow, allow organizations to tighten and accelerate the feedback loops.

There are also elements that detect “weak signals” - for instance the leading signals of Buffer Management - and enable the organization to “sense” when things start going bad.

The constant work with Psychological Flow develops the attitudes and mindsets that allow people to stay alert and sense when intervention is needed.

The effects of the Unity of Purpose and Community of Trust enables decentralized, autonomous decision-making; so that decisions can be taken the earliest moment they are necessary, without delays.

In short, an organization that is drilled with the way of working of the TameFlow Approach will be better equipped to “Sense” and “Respond” and thus to support the actions or counteractions that are needed no matter which is the Cynefin domain of concern.

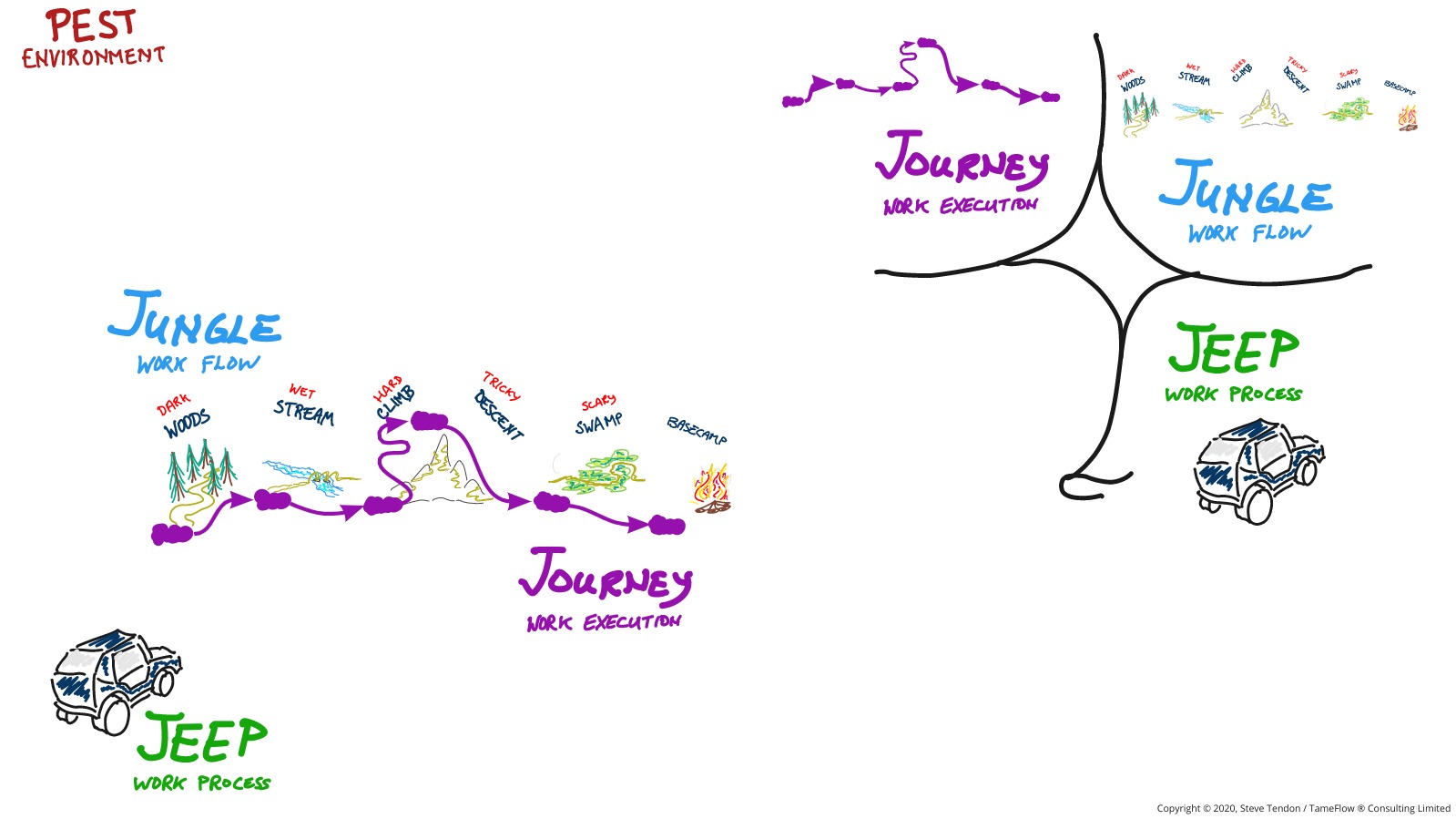

When it comes more specifcally to the “PEST Environments” (described in the Tame your Work Flow book), we observe that the elements of the Jungle, Jeep and Journey metaphor, all find a placement in the Cynefin domains.

In particular:

-

The Work Process (the Jeep) is in the Clear domain.

-

The Work Flow (the Jungle) is in the Complicated domain.

-

The Work Execution (the Journey) is in the Complex domain.

The key concept here is that no matter what process, methodology or framework is being used, reality will always present itself in all these domains concurrently. (And hopefully not in the Chaotic one, which spells out for trouble).

So even something like Scrum that is touted as designed for the Complex domain in reality has to with the fact that the definition of Scrum itself is Clear and simple; that the work that has to be done is a Work Flow that is Complicated; and that the actual Work Execution might encounter unforeseen surprises and becomes Complex.

One key distinguishing factor of Scrum is that it does not allow its own definition to evolve. Any deviation from the Scrum Guide is labeled as a Scrum “But” and is no longer considered to be “Scrum” proper. So this is an extremely rigid constraint, that does not allow the method as such to evolve any further.

TameFlow on the contrary, being deeply rooted in Patterns and Pattern Theory, has been evolving since its inception and will continue to evolve.

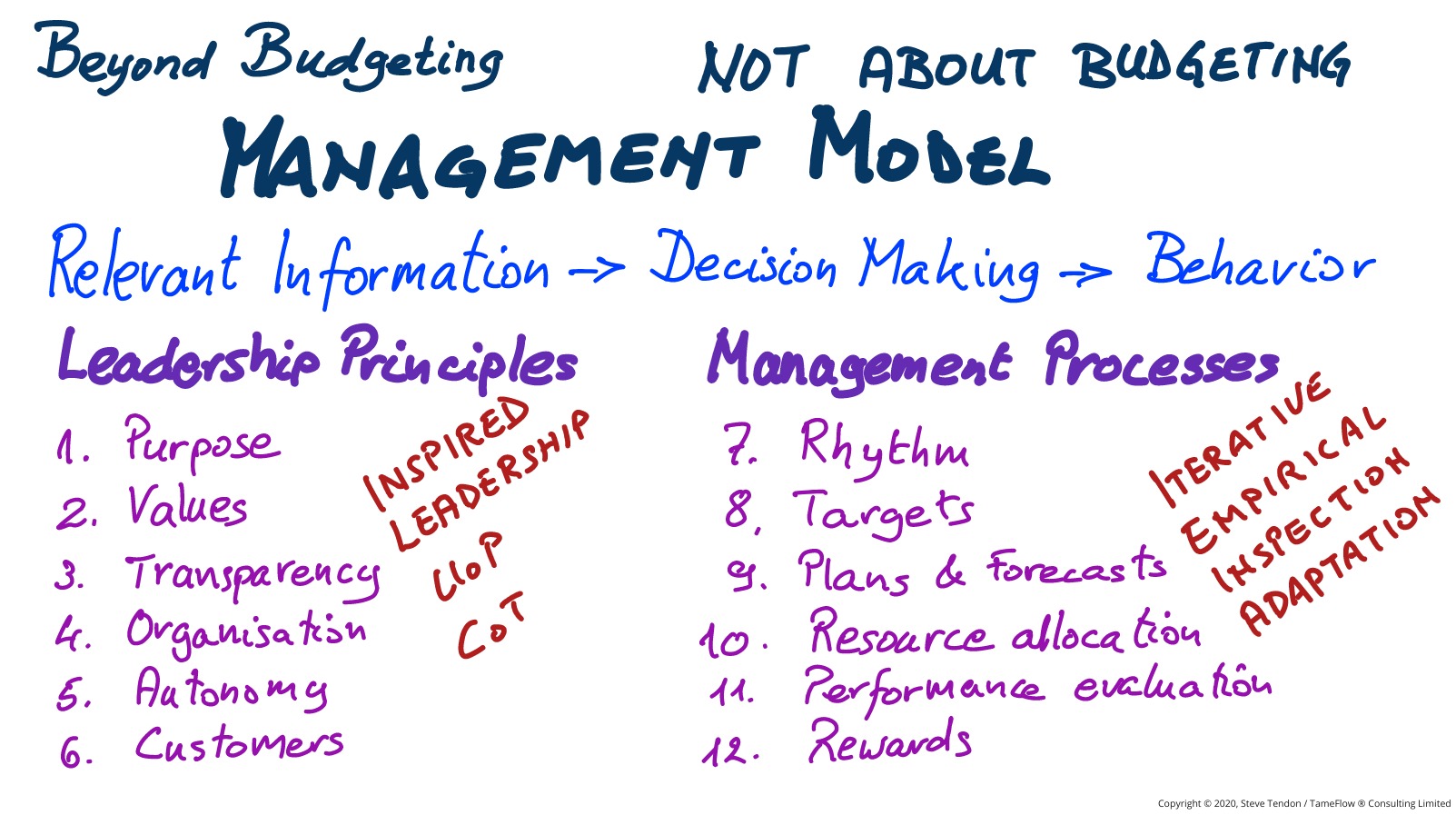

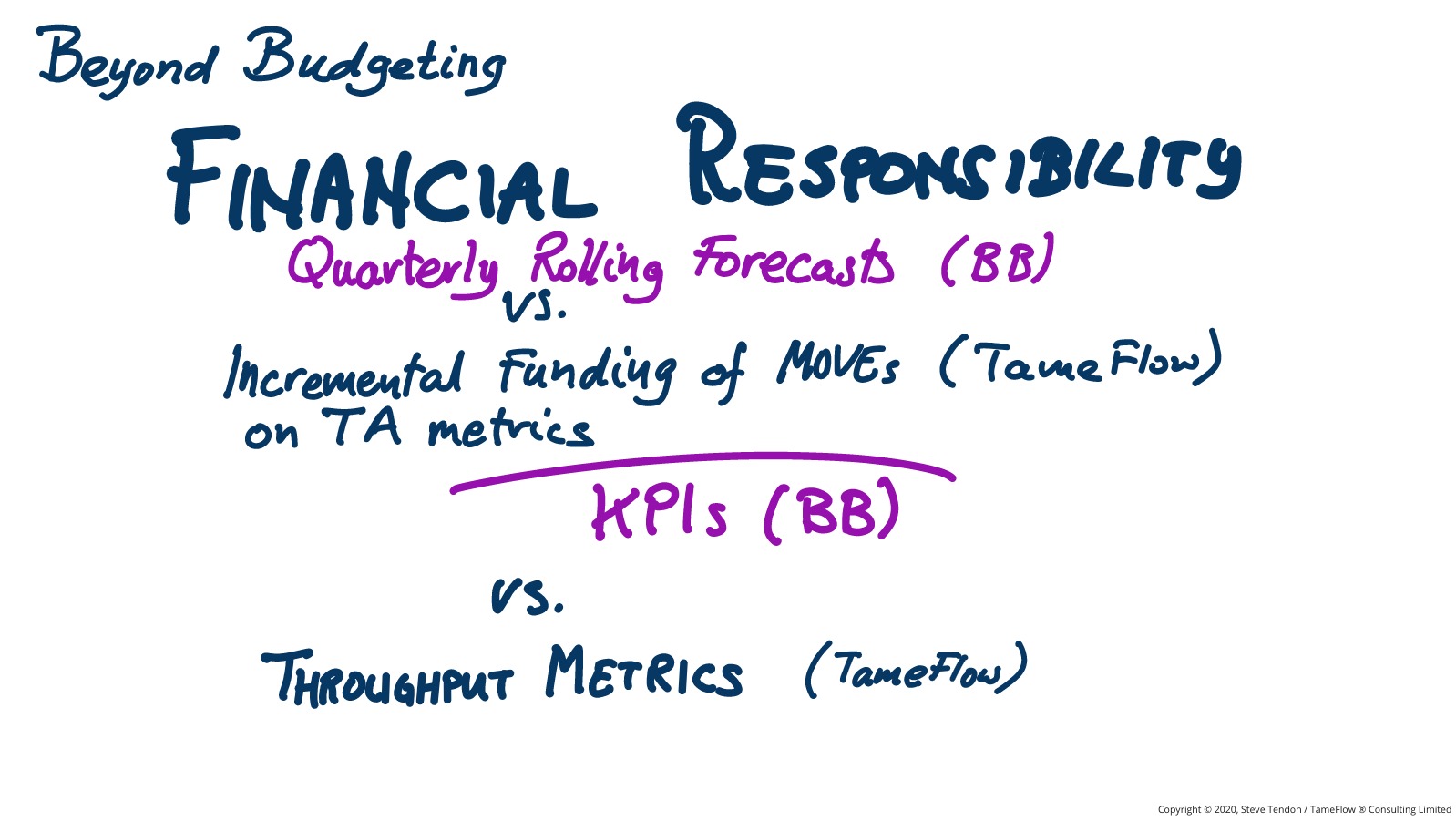

TameFlow and Beyond Budgeting

While the origins of Beyond Budgeting were clearly inspired by the practices of “Budgeting” it is better to consider the approach as a Management Model that seeks to produce relevant information supporting the best decision making which is then reflected in the behaviour of the company’s people.

In this sense Beyond Budgeting is very similar to what we do in the TameFlow Approach when using Mental Models to influence the way people make decisions.

It is noteworthy that in the “Hyper” book, the entire Chapter 7 “Budgets Considered Harmful” was about Beyond Budgeting. Effectively, Beyond Budgeting is one of the components that we use in the TameFlow Approach.

When we examine the fact that Beyond Budgeting is explained with six Leadership Principles and six Management Processes we can clearly see the connection:

-

The Leadership Principles clearly map to the foundational patterns of the TameFlow Approach: Inspired Leadership, Unity of Purpose, and Community of Trust.

-

The Management Processes correspond to the iterative and empirical inspection and adaptation that is so important for all kinds of knowledge-work.

In conclusion: Beyond Budgeting is a perfect fit for the TameFlow Approach.

However we like to use the element of the TameFlow Approach to further enhance and improve what Beyond Budgeting already does.

In particular:

-

Move beyond the quaterly rolling forecasts, and instead use the incremental funding of MOVEs on the basis of financial throughput metrics.

-

Move beyond the use of KPIs and use operational throughput metrics across the board. Notice that KPIs are always tied to silos, while throughput metrics are cross-silo; and travers the organization horizontally along its value streams.

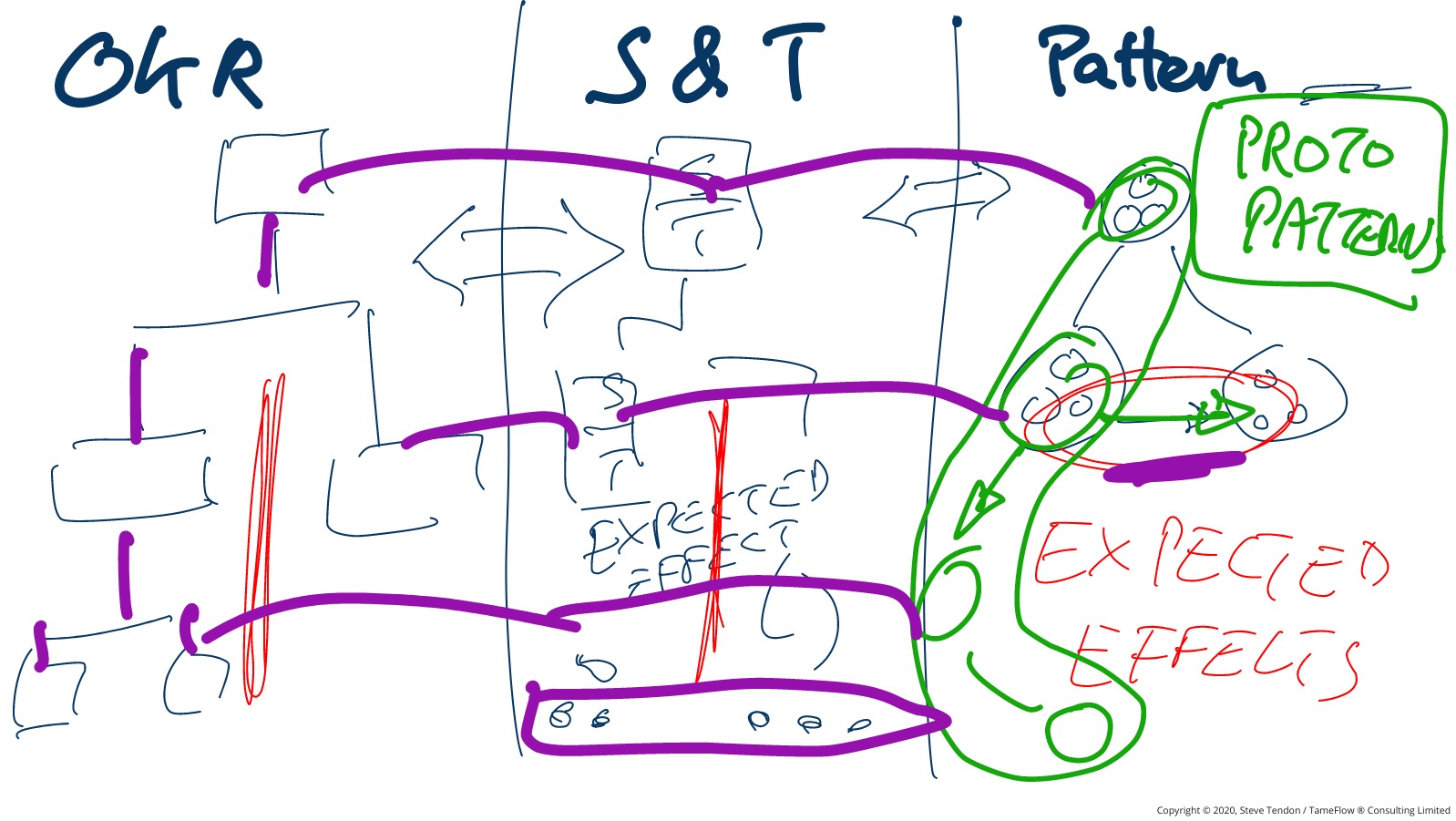

TameFlow and OKRs

Talking of silos, an additional question about OKRs was raised. While the topic has already been addressed in a webcast with John Coleman, here are some further perspectives:

OKRs can be enhanced by using the Strategy and Tactics Trees of the Theory of Constraints. The major difference is that the S&T Trees will also be specific about the actual actions that need to be performed, which OKRs leave undetermined.

Furthermore, S&T Trees also express the Expected Effects of such actions.

In the TameFlow Approach we express organizational transformations as a traversal path in a network of Patterns. Already the term makes it clear: a Pattern Network transcends the hierarchical structures of both OKRs and S&T Trees. This fact allows cross-unit actions, effectively breaking down organizational silo compartmentalization, and - for example - allowing for value stream actions to be contemplated.

The TameFlow transformational patterns, unlike ordinary Alexandrian Patterns take the idea of an Expected Effect from the S&T Trees in order to allow predetermined network traversal paths to be described. In other words, we transform the very open ended Pattern Network in a Directed Graph of Patterns. This is how the “Proto Patterns” presented in the last chapter of the Tame your Work Flow book become like recipes, cookie cutters, instructions that can be followed by someone who is not an expert in the field. The determination of a Directed Graph of Patterns provides a more powerful transformation tool than either OKRs or S&T Trees.

Bonus Post 1: The 10 Evils of Budgeting

Note: In 2013 I published two posts on Beyond Budgeting in the now defunct “Thoughts on Business” blog. Given the topic of this Campfire Talk, I repost them here.

It is often asked whether one should follow best practices when managing a business. Opinions might vary. Nonetheless, there are certain practices that are so commonly used and considered best, that no one would dare questioning them.

One such best practice is the use of budgets and the exercise of budgeting, which have been in common use since the 1920s. For sure, budgets serve noble and agreeable purposes, like:

- Conceive future plans in terms of expenses and revenues;

- Control the allocation of resources;

- Define targets;

- Motivate managers and personnel;

- Showcase the organization’s performance.

Such purposes are, normally, the concern of the finance people in companies. As early as 1952, Chris Argyris wrote about The Impact of Budgets on People wrote and showed that at “the point at which men and budgets meet,” interesting things happen. The people and roles involved in and affected by the budget, will have their own viewpoints — and often conflicting ones.

In the mid 1990s, Jeremy Hope (and his brother, Tom Hope a visiting Professor of Accounting at INSEAD), started seriously questioning the use of budgets; realizing that budgets did not provide managers with relevant information for decision making in today’s information and knowledge economy. Budgeting influences the behaviour of both managers as well as employees, in a way that is counter-productive to the business’s real goals. Budgets act as a strong conservative force, that prevent organizations from changing, as they should to keep up with the ever changing competitive environment. Why is it so? Jeremy Hope came up with the following reasons.

1. Budgets inhibit rapid response

Budgets typically happen on an annual basis, whereby expenses and revenues are estimated and used to set targets. By committing to such targets, the company sets into a straight-jacket that will hinder it from reacting to changing market conditions in a timely manner — and as we all know, in one year’s time, market conditions can change quite dramatically.

2. Budgets are too detailed and expensive

The level of micro-management forecasting required when preparing budgets are way too detailed to be meaningful. It also takes a lot of time, effort and resources to prepare the budgets. Some estimate that up to 30% of managers’ time is consumed in the annual budgeting ritual.

3. Budgets become stale

Budgets have a yearly outlook; but many forces act with a much shorter time frame. Like commodity prices, exchange rates, interest rates, customer demand, employee turnover, regulations, competitors’ actions, and so on. A yearly outlook is simply too long a time frame for any practical and effective management.

4. Budgets prevent competing successfully

For the same reason, planning on a yearly basis does not allow for the fast response and quick innovation that is necessary to compete in today’s business environment.

5. Budgets don’t support strategy

Because budgets are founded on the basic needs of business units and departments, rather than on the needs of strategic direction, they will not contribute to the pursuit of any strategy devised by top management. There are simply too many and diverse interests hidden in a budget document, and it is very unlikely that those interests are aligned with the strategic intent of top managers.

6. Budgets stifle initiatives and innovation

By their nature, budgets induce a command-and-control culture. Employees are discouraged from taking initiatives, unless they go through endless approval processes (and one year in advance!). The emergent behavior necessary for innovative thinking is replaced by conformance behavior, conformance to budget.

7. Budgets create waste

Because cost budgets have to be agreed upon on a yearly basis, budgets are a source of great wastes. In order to preserve their “spending power” department managers will try to gain approval for ever increasing costs, and then try to spend those amounts whether they are truly needed or not. Continuous improvement (like the elimination of waste promoted by Lean approaches) cannot take place effectively in organizations that are driven by budgets.

8. Budgets foment a toxic culture

Centrally-driven, hierarchical organizations with strict budgetary controls do not support transparency. Typical dysfunctions ensue, like: exploitation of employees; perceiving accountants in an adversarial manner; fending off criticism towards management; transforming the budgeting process into a sheer ceremony. Even worse effects are that all interested parties engage in endless negotiations to make the budget favorable for them. The process encourages “cooking the numbers” and “gaming the system.” It generates conflicts of interest, and a culture of mistrust and adversarial confrontation.

9. Budgets demotivate people

Unlike high performance businesses, where people tend to do better and better, budgets demotivate people. They have no incentives to exceed their predefined, yearly targets; as they would just raise the bar for themselves in the following period. Employees in a budget driven company will do the minimum to achieve their targets, and then stop there.

10. Budgets encourage unethical behaviour

Aggressive targets and exaggerated incentives can drive managers to engage in unethical behavior, in order to reach their targets at any cost. Budgeting is what allows for “creative” accounting scandals (like Enron), which can seriously damage a company’s reputation, or even put it out of business entirely.

In conclusion, budgets have many problems. Therefore, the next time you set out to make a budget, ask yourself: is it really worth it? or shouldn’t you maybe find better ways?

Bonus Post 2: The 5 Budgeting Games You Do Not Want to Play

It is common to desire creating a high performance business. Often, you will find yourself making comparisons with the world of sports, especially when invoking the metaphors of team and team work. Who doesn’t want to be on a good team? a high-performance, winning team?

High performance organizations, like good teams, are distinguished by having a Unity of Purpose and a Shared Vision. Management often announces pompous “vision statements,” in the hope to instill these sentiments.

Then they get entrenched and engaged in making… budgets!

The earlier post, The 10 Evils of budgeting, highlighted how budgets and budgeting bring with them many negative aspects. Some of these detrimental characteristics are more obnoxious than others, in particular those that create a toxic culture that can even induce unethical behavior.

There will be many hidden agendas in between the lines of a budget, as all interested parties engage in endless negotiations to make the budgets favorable for themselves. Budgets, by their nature and the ways they are used, are not even capable of creating Goal Congruence amongst all involved parties — let alone the noble sentiments of Unity of Purpose or Shared Vision.

The conflicting interests are not surfaced. In most companies, it is even “not politically correct” to talk about these conflicts in the open; they are effectively taboo topics. Yet, these conflicting interest and hidden agendas, while shielded by ceremonious politeness, are there! They might remain concealed in the budgeting process, yet they give rise to very evident behaviors, attitudes and ways of thinking that give a way the noxious culture.

In particular, these hidden agendas result in Budgeting Games, where each and everyone tries to get an advantage over the other… ehm… “teammates”!

In an article published in 2006, Forecasting the End for Budgets, Peter Bartram identified the following five typical “games” that managers engage in when the have to work with budgets.

The Sky is the Limit!

Managers will fight tooth and nail to get as large a budget as possible; “just-in-case…”, so that they are covered for any contingencies that might happen. A more reasonable behavior would be to ask realistically for what is needed, with the knowledge at the time, rather than speculating (crystal ball gazing) about unknown, future possibilities.

Mine is Bigger than Yours!

Managers measure each other’s ego-boosting status inside the company according to the size of their budget. Rather than focusing on who creates the greater value, the company culture recognizes tacit entitlement to the biggest spender. Oh, yes!, then they engage in a multitude of “cost savings” programs. Each manager will want the others to pay their dues in the battle against soaring cost, while they will just have to have a bigger budget for themselves.

Cooking the Books

This happens, for example, when revenue declaration is delayed at those times when budgeted targets have been met, so that the excess revenue can be used for future targets instead. The objective is meeting the numbers consistently, even at the detriment of exceeding and going beyond the goals. When all managers engage in this behavior, the potential growth of the business is artificially limited to the shortsightedness of the budgets.

Hey Big Spender!

Managers feel compelled to spend the whole of their budget; otherwise it is customary that they will see it cut the following year. Budgets seem to suffer from some variant of Parkinson’s Law: the expenditures inevitably grow to match the budgets that are initially allocated. In this kind of culture, those who by virtue are able to achieve their goals and spend less, will be punished by getting less resources. Shouldn’t they be the ones who have access to more resources, after demonstrating that they can mange resource wisely?

Bonus or Bust

Managers pay more attention to the metrics that determine their own salaries or bonuses, rather than focusing on targets that actually benefit the business. Their self-interest is simply not aligned with the best interest of the business.

All these games invariably create conflicts of interest, tensions, and a culture of mistrust and adversarial confrontation, which is in stark contrast with the very idea of building a high performance organization, a team with unity of purpose, and teamwork inspired by a shared vision. This is one of the primary reasons why companies engaging in conventional budgeting practices will never be able of exhibiting high performance traits, if not (maybe) by some lucky strike of coincidence.

What about your company? Are you using budgets? If so… are you surprised if you have just average results?

If you found the topics in the “Campfire Talks with Herbie” interesting, there is much more to learn about them in the The Book of TameFlow book.